Dynamic Cash Flow Projections » Document Assumptions

The Purpose of Document Assumptions

While financial projections are estimates of business transactions of the future, they are firmly based in the business realities of the past. In order to project how the company’s performance will look like tomorrow it will be important to review all the assumptions that went into shaping the events of today and yesterday.

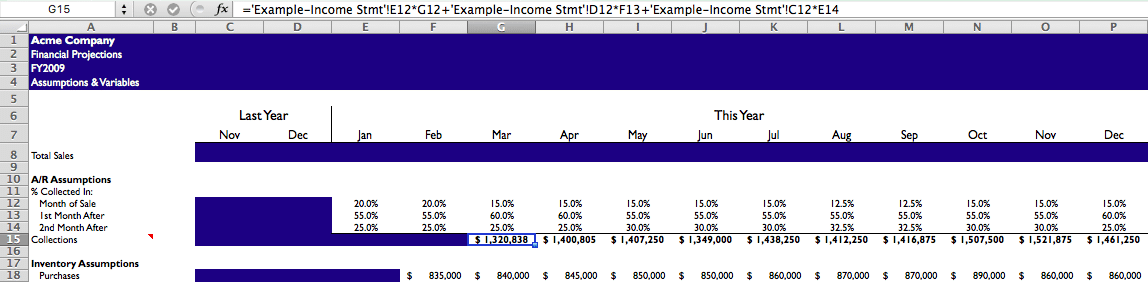

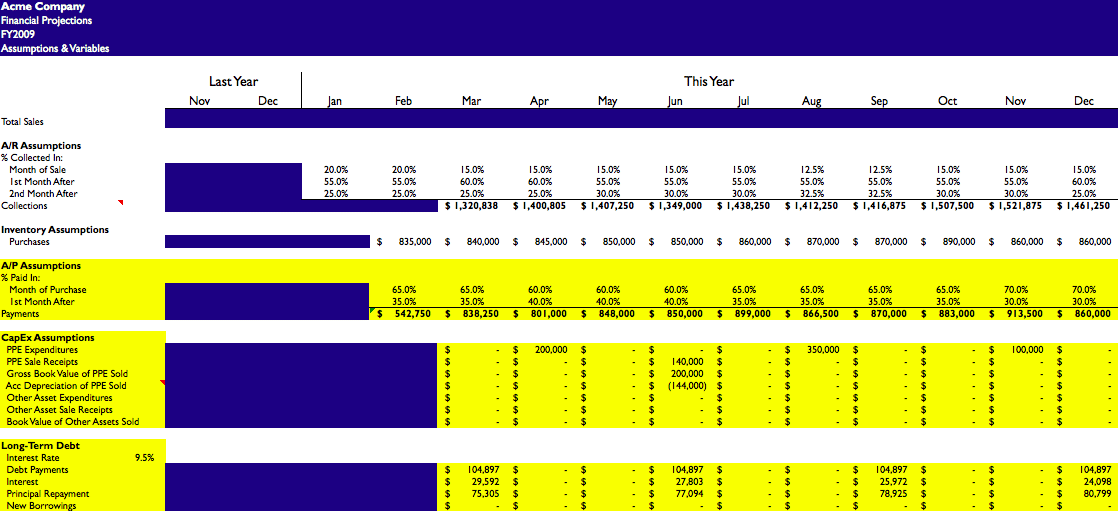

The objective of the assumption page is to have an input page that serves as a reference for the financial projection. Done correctly, you only need to enter numbers once into the assumption page.

Make sure each number is entered into its own cell.

Then, just reference that particular cell any time a formula is entered. This allows you to easily see the effects of changes to your assumptions instead of wasting time trying to find which formulas it applies to and in which spreadsheet.

You may end up adding additional assumptions to the assumptions sheet. That’s ok. While you don’t want to make this model overly complex, you do want to enable yourself to change key variables quickly. Remember, when you are building the projection, you want it to reflect your best guess of where the business is headed and not just the rosiest possible scenario.

The point of implementing the Dynamic Cash Flow Projection in your company is to enable yourself to identify problems before they occur and taking steps to avoid those mistakes or lessen their impact. It will do your company no good to pretend a potential problem doesn’t exist simply because you can dream up some good looking numbers. In addition, it won’t help your credibility with external parties such as banks and investors if they find your projections are frequently too optimistic.

How Often To Document Assumptions

Documenting assumptions is a continuous work in process. Things will change all the time. Take certain assumptions away, while you will add others later. Expect to make frequent updates to this page.

Remember, this is a projection, not a budget.

You will be changing your assumptions to reflect current business realities as you progress through the fiscal year.

Who Documents The Assumptions

The assumptions page has inputs from all parts of the business. It may be necessary for the CFO/controller updating or creating the spreadsheet to go to various departments to get their input on various subjects:

- Revenue

- Cost of Goods Sold

- Overhead Expenses

- Capital Expenses

- Inventory and Work-in-Progress

- Debt Obligations

- DSO

- DPO

- Cash Conversion Cycle

How To Document The Assumptions

As described above, it may be necessary to discuss future growth assumptions with a representative from different parts of the business. Look at the following questions you need to ask when documenting the assumptions.

Sales:

- Ask them what their growth projections are.

- How many units do you forecast to sell?

- By what % do you forecast growth to occur? (this is the easiest way to ask)

Operations:

- Ask them what their growth projections are.

- How will costs for inventoried items and raw material change in the next 12 months?

- Do you foresee any shortages or excess capacities?

- Will there be any changes in price or payment requirements?

- What sort of capital expenditures are there for the next 12 months?

- What percentage of raw material gets turned into Work-in- Progress (WIP)?

Finance/Accounting:

- Ask them what their growth projections are.

- What are the notes that the company is obligated to pay?

- How much do we pay each month in total for debt? How is it broken out?

- What is the relationship between accounts receivable versus sales? Is there an average percentage of sales that you can use?

- What is the relationship between accounts payable cash disbursement?

- When do we pay?

- What percentage of raw material gets turned into Work-in- Progress (WIP)?Once you have gathered up all this information, put it down on an Excel worksheet titled “Assumptions”.

Remember to enter in numbers into their own individual cells.